In FE fundinfo’s annual adviser survey, we discovered that three quarters of advisers believe that either a 3% or 4% annual drawdown rate would be sustainable – this was against the backdrop of rising interest rates and inflation. The same survey also revealed that sequencing risk – a market fall early in retirement reducing the length that a portfolio will last – is still seen as the biggest risk a client can face, according to advisers.

The FCA recently released its Retirement Income Data and the latest figures give us an interesting view of the current retirement landscape. The data looks at trends in pension withdrawal rates, DB to DC pension transfers received as well as the use of advice when clients purchase retirement products, amongst other metrics. The regulator has collected this data since 2015 and they reveal insights into consumer behaviour and retirement income patterns.

Whilst drawdown (especially post-Pension Freedoms) has allowed clients to have more flexibility in how they access their retirement income, it requires the help of advisers and some financial planning.

What does the data say?

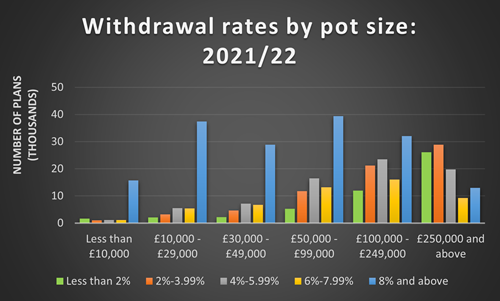

According to the FCA data, drawdowns saw an increase of 24% from 2020/21 to 2021/22 and the total number of pension plans accessed for the first time increased by 18% over the same period. 40% of regular withdrawals were done at an annual rate of over 8% of the pot size for the most recent year. The use of regulated financial advice and guidance, when making full withdrawals, marginally increased to 35% for the recent year; it stood at 33% for the previous year.

Source: FCA Retirement Income Data ; October 2022

Annuity sales also witnessed an increase and this can be attributed to the attractiveness of rising interest rates. Some advisers see a combination of annuities and drawdown as an option for retirement going forward.

No retirement plan will ever be risk free. Moving to a decumulation approach essentially replaces one set of risks with another. Whilst some investors may think it counterintuitive to increase their risk exposure as they approach retirement, in a decumulation portfolio, the bigger risk might be running out of money rather than the value of an asset falling. More needs to be done to empower advisers with innovative investment solutions that help with client conversations and their retirement planning and move away from models and strategies which have perhaps run their course.

Drawdown is complex and there is no “perfect” solution to mitigate the challenges clients will face in retirement; having a robust process in place whilst maintaining a flexible outlook and approach is useful to anticipate, and react to, changing events as they occur.

How can FE Investments help?

At FE Investments, we aim to provide advisers with the support they need to advise their clients effectively and suitably. Our decumulation proposition is structured to help mitigate the risks specifically associated with retirement, such as sequencing risk and shortfall risk.

Our portfolios cover a wide spectrum of outcomes to ensure clients have enough choice of the types of investments they’d like to make, along with choice over the amount of sustainable principles in their portfolio. Our Hybrid, Income and Mosaic portfolios emphasise risk management and are commonly used in the accumulation phase of life. In contrast, the Decumulation portfolios combine two approaches to risk management in order to provide a broader view of retirement needs.

Important information

This is a marketing communication, intended for professional advisers only. Not for use by retail investors. It is not intended as a recommendation to buy or sell any particular asset class, security or strategy. The value of investments and the income from them may go down as well as up and you may not get back the amount originally invested. All information is correct as at the date of publication unless otherwise stated. Where individuals or FE Investments Ltd have expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

This communication contains information on investments which does not constitute independent research.