What is the Lifetime Allowance?

The pension Lifetime Allowance (LTA) is the maximum amount of money that clients can save in their pension without paying extra tax when they withdraw it. It has been criticised by some for being unfair, complex and discouraging people from saving enough for retirement.

The current LTA is £1.07 million, which means that if a pension pot is worth more than that, clients will have to pay a tax charge of 25% or 55% on the excess amount, depending on how they take it out.

The LTA was introduced in 2006 and has been altered several times since, with a high of £1.8 million introduced in 2010, and a low of £1 million in 2016. The LTA has been unchanged for the past 4 years after being frozen at £1.07 million in 2021.

In a bid to boost the UK workforce after an increase in economic inactivity since Covid-19, the government announced plans to remove the LTA in the 2023 Spring Budget. Whilst the charge was removed in April 2023, the LTA will be abolished entirely this coming Spring and replaced with two new limits: a Lump Sum Allowance and a Lump Sum and Death Benefit Allowance.

How will the removal of the LTA affect retirement planning?

The removal of the LTA will have an effect on many of your clients, whether they are in the accumulation or retirement phase. Whilst the specific implications on each of these segments will be discussed below, the common effect is likely to be that clients will want guidance on how these changes will individually affect their plans and goals.

Clients in accumulation

The removal of the LTA will have a significant impact on those still building their pension pots, especially for higher earners and those who have been saving for a long time. It will mean that they will be able to save more in their pension without worrying about the tax implications, and potentially enjoy a higher income in retirement.

The removal of the LTA, coupled with the 50% increase in Annual Allowance, gives saving for retirement a significant boost and may likely require current financial plans to be tweaked in order to ensure that contributions and tax free allowances are optimised.

Clients in the retirement phase

Whilst at first glance the removal of the LTA may seem like a simplification in complicated pension tax regulation, in reality this is unfortunately unlikely to be the case. The biggest complexity comes for those clients who have already accessed their pension. In these cases, clients will need highly personalised advice to work out their new allowances and make any necessary adjustments to their current financial plans.

Another angle to consider is the effect that the LTA had on how the pension was invested. If investment growth was limited to avoid tipping over the LTA and incurring hefty tax charges, the removal may require a change in investment strategy to more accurately represent the risk appetite of the client. This may affect current cashflow models that will subsequently need updating to reflect potentially higher returns.

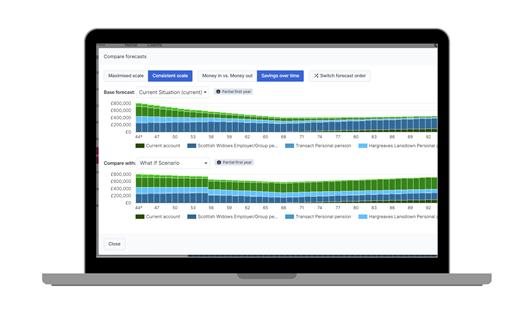

Making the most of cashflow modelling for retirement planning

Cashflow modelling is an integral part of the advice process, allowing potentially complicated plans to be visualised in a client-friendly and intuitive way. The removal of the LTA theoretically makes cashflow modelling for retirement easier, with no need to contend with changing thresholds and potentially large tax charges.

Especially in times of uncertainty (such as large changes in pension tax legislation), visual cashflow plans give clients reassurance over their financial futures, and help them to understand and engage with their retirement planning.

By using a range of graphs and scenarios, you can show your clients how their pension pots will grow and shrink over time, how their income and expenditure will change, and how different factors, such as inflation, market fluctuations, or life events, can affect their outcomes.

This can help your clients to see the impact of their decisions, and to compare different options and strategies to make informed choices to achieve their financial goals.

The bottom line

The removal of the LTA will be welcomed by high earners and those close to the current allowance, however the introduction is likely to cause initial complexity for advisers with clients who are already in the retirement phase and have accessed their pension.

In regards to the effects on retirement planning, it is likely that many clients will want to review their current plans and make adjustments to ensure they are optimising the allowances available. Cashflow modelling will prove valuable in visually demonstrating the effects these changes will have on financial goals, and enable clients to make informed decisions about their retirement planning.